Wesley Gee Talks Disclosure: Making the Most of Materiality

Our director of sustainability, Wesley Gee, visited New York to share insights as part of an expert panel at IR Magazine’s Environmental, Social and Governance (ESG) Integration Forum in December. In the second part of our followup interview, we discuss how to think about materiality for ESG, emerging ESG reporting standards and how IROs can adapt to ESG issues.

How do companies look at materiality in the context of ESG?

Financial implications (business viability) should always come first, but with a longer-term lens than is typically used by investor relations teams. The topics considered for ESG materiality are relatively wider reaching, and the stakeholders engaged are more diverse since there is a need to address analysts, investors and social licence influencers. Unfortunately, assessments are sometimes conducted solely to inform the content of the report, which is a missed opportunity when so much more can be learned about improving governance, engagement and measurement within the organization.

How should companies assess making disclosures that are not material?

Consider providing this information on the website, where it doesn’t require the same degree of rigour to disclose. For specific topics, information related to management approach can be shared along with stories that don’t need to align with a framework. We sometimes see these less critical topics in reports as emerging issues or as stories – but it can make reporting long-winded. So either put this information on the website or respond to external surveys (e.g., CDP, DJSI) that touch on these issues. Creating an encyclopedia tells your reader that you are not focused. Your reporting should remain succinct, while surveys can be used to meet the specific needs of a niche sector organization.

What are the strengths of the various ESG standards?

The Global Reporting Initiative (GRI) is still the most wide-reaching industry standard for sustainability reporting. (Our reporting trends research shows about 84% of companies reported in accordance with the GRI Guidelines or Standards in 2018.)

Although companies have tended to take longest to adopt the Sustainability Accounting Standards Board (SASB), more of them are participating (14% in 2018) as the scope expands from a US-centric to a global perspective.

In its first year, the Task Force on Climate-related Financial Disclosures (TCFD) has many companies taking a light approach to the recommendations (32% acknowledging them in 2018), with only a few offering climate change scenarios.

The Sustainable Development Goals (SDGs) engage with communities and people most broadly, though we need to be careful in assuming they can be meaningfully applied by investors.

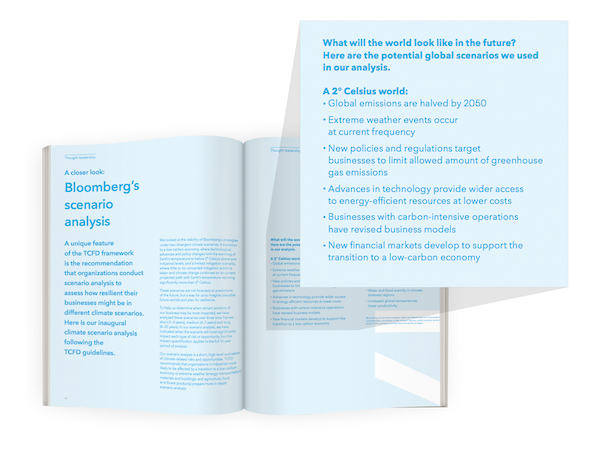

Of the companies included in our 2018 Trends sample, Bloomberg presented one of the most robust applications of the TCFD guidelines. It included scenario analysis: a short, high-level evaluation of climate-related risks and opportunities against specific potential outcomes.

Are IR professionals and other non-specialists equipped to engage on ESG matters?

Investor relations officers (IRO) at some companies are becoming more sophisticated in ESG so that they are able to remain on top of a wider range of issues. They are considering integrated reporting as a way to show genuine strategic alignment. But plenty of IROs dismiss the value of ESG on their calls because they lack understanding of the issues falling under “ESG” – and they sometimes lean hard on sustainability officers to address a growing number of requests.

What engagement practices are companies using?

IROs sometimes use materiality assessments to understand the priorities and expectations of analysts, investors and other key influencers; and, ideally, sustainability/ESG practitioners can piggyback on existing IR engagements. A great way to get data and context is to engage analysts and investors before and during investor days, using online surveys and in-person sessions to get to the heart of key influencer priorities and expectations. The report and website are a common reference point that stakeholders can view before formulating opinions, so it’s important for reports to provide helpful information on strategy, purpose, performance and proof points.

Check back for the third part of our interview, where we discuss how and when to make ESG/sustainability disclosures.